GT Advanced Technologies is the company Apple had partnered with to produce sapphire displays for it’s smartphones and who recently filed for chapter eleven bankruptcy. Some of the sensational accusations that GTA has made against Apple have been covered by the financial media and I’ve also seen speculation that GTA would have gone bankrupt anyway even without the Apple deal. It appears that most of GTA’s revenue (~one billion/year) was derived from solar equipment revenue that collapsed in 2013 when certain subsidies expired.

However, I thought it might be interesting to discuss how a company evaluates such a huge decision and the importance of financial modeling.

However, I thought it might be interesting to discuss how a company evaluates such a huge decision and the importance of financial modeling.

If GTA’s CEO, Tom Gutierrez, was smart, he commissioned his finance people to begin constructing a financial model of what the company would look like in the future if they signed a deal with Apple. Then the model would be compared to an alternate view where the company doesn’t sign a deal with Apple. In a cost/benefit analysis, only the incremental profit is used. A slide showing that after a five year deal with Apple that they would rake in $5 billion in profits is a lot less impressive if they would earn $4 billion anyway without the deal. It sounds like a given that this would be done, but it wouldn’t surprise me if GTA didn’t really have a good handle on the numbers. This kind of modeling takes a lot of time and effort and in the heat of negotiations, often shortcuts are taken which can lead to disastrous results.

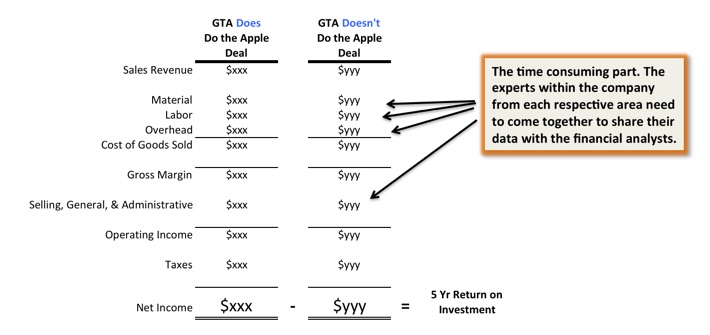

So what should have taken place? First, the group negotiating the deal with Apple would give finance a clear direction on what future volumes to expect. It always starts with volume. Then the finance group will take those volumes to all the internal departments to get an estimate of any incremental additions and subtractions on the yearly income statement.

So what should have taken place? First, the group negotiating the deal with Apple would give finance a clear direction on what future volumes to expect. It always starts with volume. Then the finance group will take those volumes to all the internal departments to get an estimate of any incremental additions and subtractions on the yearly income statement.

- Purchasing – What will incoming raw materials cost?

- Manufacturing Assembly –New hires? Square footage needs? Additional buildings? Yield & Scrap issues?

- Manufacturing Engineering – What kind of tooling & machinery will you purchase? Future warranty costs?

- Logistics – Outbound freight costs will be what? Are distribution assets adequate?

- Administration – Any incremental order fulfillment or customer service costs?

This data-gathering stage is the danger zone where companies often get into trouble. No one wants to wait for good information and least of all impatient CEO’s. Gateway Computers shocked the world in the early 2000’s when they offered a 42” plasma TV for the than unheard of price of two thousand dollars. I still remember the excitement in the air when our Director of Manufacturing called a plant employee meeting and let the cat out of the bag that we were going to be assembling plasma TV’s. Gateway’s CEO had inked a deal before a proper financial model had been completed, and the yield scrap and customer support issues boomeranged on us so hard it almost killed us. It turned out that there was good reason that no one else at the time could even come close to our price. We were losing two thirds of our plasma TV’s to yield issues at the time, and our customer returns were through the roof.

Assuming that GTA had a good financial model of what to expect in terms of future revenues and expenses (if they even made it this far in the analysis), they would then compare their estimated future profits to a scenario in which they didn’t do the deal. So if GTA would earn $5 billion in profits, they must deduct the $4 billion they would have earned anyway. So only the $1 billion in incremental profit counts in the analysis.

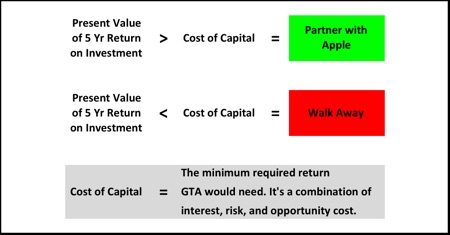

But wait, that’s not all. A billion dollars in the future is worth less than a billion dollars today. GTA would have to buy those furnaces today with more valuable present day dollars. So that billion dollars of profit over five years is then discounted back to present day value, which will make it a lower number. NOW we can make our comparison.

Assuming that GTA had a good financial model of what to expect in terms of future revenues and expenses (if they even made it this far in the analysis), they would then compare their estimated future profits to a scenario in which they didn’t do the deal. So if GTA would earn $5 billion in profits, they must deduct the $4 billion they would have earned anyway. So only the $1 billion in incremental profit counts in the analysis.

But wait, that’s not all. A billion dollars in the future is worth less than a billion dollars today. GTA would have to buy those furnaces today with more valuable present day dollars. So that billion dollars of profit over five years is then discounted back to present day value, which will make it a lower number. NOW we can make our comparison.

So if GTA has to spend a total $500 million dollars to do the deal and they require a 30% return on investment, does the discounted profit exceed $650 million? That’s the simple equation it all comes down to.

I’ve worked with financially disciplined companies who use this methodology when evaluating potential new products, building new distribution centers, or investing in new manufacturing technologies so this is not any earth-shattering, new voodoo. It just takes time, a lot of it.

I’ve worked with financially disciplined companies who use this methodology when evaluating potential new products, building new distribution centers, or investing in new manufacturing technologies so this is not any earth-shattering, new voodoo. It just takes time, a lot of it.

RSS Feed

RSS Feed